You can count on it. When the Federal Reserve changes its interest rate, news headlines about mortgage rates will follow.

This cycle unfolds up to eight times a year, so many home shoppers get the idea that the Fed regulates mortgage rates.

Fed decisions affect mortgage rates, but the Fed doesn’t control mortgage rates directly. In fact, the Fed’s actions can have unpredictable effects on the rates new home buyers pay on their mortgage loans.

Does the Fed set mortgage interest rates?

The Federal Reserve is the most powerful financial institution in the U.S., and its decisions reverberate throughout the global economy, including the mortgage market.

When the Fed adjusts rates, it’s changing the Federal Funds Rate, which is the overnight interest rate banks charge each other when they lend reserve funds to manage their cash flow. This rate influences short-term borrowing costs throughout the economy, including rates on credit cards, auto loans, and home equity lines of credit (HELOCs).

But 30-year fixed mortgage rates are long-term rates. They’re shaped mostly by broader financial markets, not by the Fed’s policy committee.

What actually drives 30-year mortgage rates

Mortgage rates are closely tied to:

- U.S. Treasury yields, especially the 10-year Treasury

- The price of mortgage-backed securities (MBS)

- Inflation and jobs data

- Predictions about future economic growth

- Demand for U.S. bonds globally

- Risk premiums required by investors

All this affects mortgage rates because a single home loan doesn’t exist in an economic vacuum. After a borrower closes a mortgage loan to buy a primary residence, the lender will often sell this loan into the secondary market.

Multiple mortgage loans get combined into mortgage-backed securities, a financial asset investors can buy and sell. Investors who buy mortgage-backed securities expect returns that compensate them for inflation risk, interest-rate risk, and the chance borrowers refinance earlier than expected.

Because of this expectation, mortgage rates come with future risks and payoffs already built into their pricing. The rate you pay on a home loan this month reflects what investors believe will happen to inflation, economic growth, and Fed policy over the next few years.

How do mortgage rates react when the Fed lowers its rate?

When the Fed cuts the Federal Funds Rate, as it did three times between September and December, many borrowers expect mortgage rates to fall immediately. Sometimes rates do fall, but not always.

One reason for this: The mortgage markets have usually priced in the Fed cut before it happens.

If investors expect the Fed to lower its rates, they react to that expectation before it happens. That’s why Treasury yields and mortgage rates often fall before the official announcement from the Fed.

When the Fed does act, mortgage rates may barely move, or they may even rise if the cut was smaller than markets expected.

Why mortgage rates sometimes rise after a Fed cut

Mortgage rates can increase after a Fed rate cut if:

- Inflation still looks stubborn

- Employment data is strong

- Investors expect rates to rise again later

- Bond markets sell off due to higher demand for stocks

When one or more of these market forces line up, investors may expect higher yields on long-term bonds. This pushes mortgage rates upward even as short-term rates fall.

Comments from the Fed chair about the future of the economy can also cause a mortgage rate increase.

For example, after the 0.25 percent cut in October, Fed Chair Jerome Powell said more cuts in December were not a foregone conclusion. Markets reacted with a temporary mortgage rate increase, despite the Fed rate cut.

Again, mortgage rates reflect the future outlook of the economy; not its present conditions.

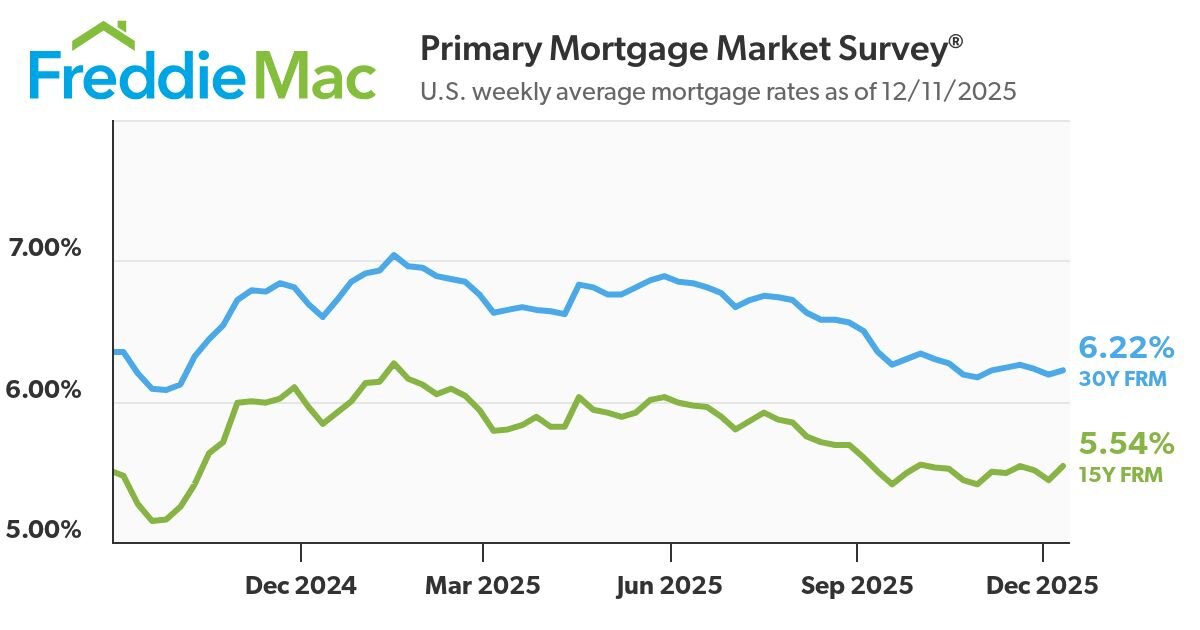

Will mortgage rates keep falling in the wake of the Fed’s 2025 cuts?

The Federal Reserve lowered the Federal Funds Rate by 0.25 percent three times during the last four months of 2025. Investors anticipated each of these cuts, and they were proven right each time the Fed’s governors gathered for a meeting.

In the months leading up to the Fed’s late-2025 rate cutting campaign, mortgage rates had already started to adjust downward as investors priced in slower economic growth. By the time policymakers acted, much of the impact had already been absorbed by financial markets.

This dynamic helps explain why mortgage rates did not plunge dramatically even as the Fed cut its benchmark rate by a total of 0.75 percent between September and December.

As for 2026? Many economists think rates could continue declining gradually, possibly falling below 6 percent for the first time since September of 2022. Of course, future economic shifts could change these forecasts.

How are tariffs and other instability affecting mortgage rates?

Mortgage rates follow a reasonably predictable cycle:

- A strong economic outlook pushes mortgage rates higher.

- A weak economic outlook puts downward pressure on mortgage rates.

What’s harder to explain is how mortgage rates react to uncertainty about the future, and uncertainty has been the hallmark of the 2020s.

First, the Covid-19 pandemic interrupted what may have been a period of rising mortgage rates in 2020 and 2021. Instead, as the economy shut down, mortgage rates set historic lows. Then, inflation set in, sparking an aggressive campaign of rate increases by the Fed in 2022 and 2023.

Now, during the second Trump Administration, tariffs have put pressure on pricing, causing worries about inflation.

If investors believe tariffs will keep inflation above the Fed’s target, mortgage rates may remain about the same even during the Fed’s rate-cutting cycle that’s now underway.

Along with tariffs, economic instability can come from:

Labor markets and wage growth

Strong wage growth is good for households, but it can also worry bond markets.

If wages rise faster than productivity, inflation risks increase. This can keep mortgage rates elevated, regardless of what the Fed does in the short term.

Government borrowing and bond supply

Large federal deficits translate into more bonds in the marketplace. This elevated supply can push yields higher. Mortgage rates often rise alongside Treasury yields in these conditions.

Global instability

Overseas investors also affect U.S. mortgage rates. Economic instability abroad can push more money into the relative safety of U.S. bonds, lowering mortgage rates. Strong growth globally can pull capital away from U.S. bonds, raising rates.

What Will Happen to Mortgage Rates in 2026?

No one can predict mortgage rates with certainty, but we can focus on the forces that are likely to shape rates.

If economic growth cools in 2026:

- Inflation pressures may ease

- Bond yields could drift lower

- Mortgage rates may gradually decline

This could be more of a normalization scenario than a dramatic rate drop.

Why a return to ultra-low rates is unlikely

The sub-3 percent mortgage rates seen earlier in the decade were a product of extraordinary conditions:

- Near-zero short-term rates

- Massive Fed bond-buying programs

- Pandemic-driven economic shocks

Unless we experience a severe recession or financial crisis, mortgage rates are unlikely to return to those levels.

What all this means for borrowers

How do everyday home buyers navigate this global tapestry of forces that shapes mortgage rates? Rarely by reacting to the Fed’s moves, regardless of what news headlines say.

Instead, home buyers and refinancing homeowners can create their own affordability by controlling what they can control: their personal finances.

The news reports average mortgage rates. A borrower’s personal finances pinpoint where their rate will fall within the context of this average rate.

Borrowers with:

- larger down payments (or more home equity for refinancers)

- higher credit scores

- lower monthly debts

- job stability

can often qualify for lower-than-average mortgage rates which can lead to lower monthly payments.

A mortgage calculator helps borrowers see how a monthly mortgage payment works.

A mortgage preapproval can show how your personal finances work together with global economic forces to shape your rate. Better’s preapproval can show an estimate in as little as three minutes.

...in as little as 3 minutes – no credit impact