What you'll learn ✅

Whether moving costs are deductible on your federal tax return

Which tax deductions for moving expenses you may qualify for

How employer reimbursements and old rules fit into today’s tax code

How to file deductions using IRS Form 3903

Whether you’re moving across town or across the country, out-of-pocket costs add up fast. This can be a budget strain, so many homebuyers wonder if moving expenses are tax deductible under current federal rules. For most taxpayers, they aren’t.

Only a narrow few can still claim the deduction, and the criteria are very specific. Read on to understand today’s requirements so you can save for a future purchase confidently.

Are moving costs deductible? The current rule

Under current federal law, only members of the armed forces on active duty who relocate because of a permanent change of station (PCS) can deduct moving costs on their taxes. Intelligence community employees moving in 2026 or later also qualify.

This policy stems from the Tax Cuts and Jobs Act (TCJA) of 2017, which suspended moving expense taxes for most Americans from 2018 through 2025. The One, Big, Beautiful Bill Act (OBBBA) made this change permanent on July 4, 2025.

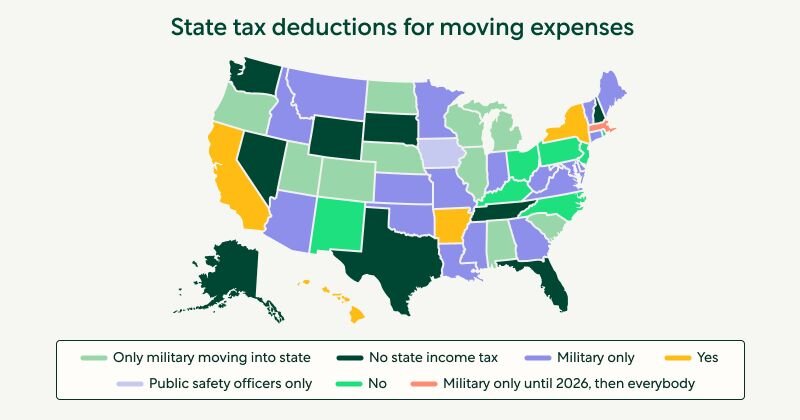

State-level deductions

Many states conformed to this bill in its entirety. However, some have chosen to decouple from a few of the OBBBA’s provisions. These states still allow moving expense deductions for job-related moves — not just for military households.

Check your state’s instructions to see what applies to your move and whether additional paperwork is required. Here’s a quick reference map to see if your state has exemptions.

What are qualified moving expenses?

Qualifying taxpayers can only deduct certain expenses. These costs must be directly related to transferring household items and family members from one home to another, such as:

Transportation of household personal items like professional movers, truck rentals, and similar services

Packing and shipping expenses like boxes and tape, plus paid services to pack or crate items

Temporary storage of belongings while in transit, up to 30 days

Traveling to the new residence, including transportation and lodging costs for you and your household

Insurance for goods in transit or storage, covering costs if anything is damaged or lost during the move

To qualify for tax deductions, expenses must be unreimbursed. This means you pay out of pocket for these costs and don’t receive any related refunds from your employer or the government.

What moving expenses aren’t deductible?

The law restricts many costs that people associate with moving. Here are the main moving expenses that aren’t tax deductible:

Real estate transaction costs, including commissions, attorney fees, and transfer taxes

House-hunting trip expenses, such as the travel and accommodation costs you accumulate while searching for a new home

Costs for short-term housing while you wait to move into a permanent residence

Food and drink purchases while traveling

Home improvements to ready a house for sale or renovate a new residence

Updating personal documents, including fees for a new driver’s license or vehicle registration

Losses from selling or donating goods, such as selling items at a discount or giving away belongings before a move

Amounts reimbursed by the government or an employer

Some closing costs, such as appraisal and title service fees

Keep in mind that some closing costs are tax deductible, like origination fees and prepaid property taxes, so it’s best to ask a tax professional for detailed advice.

Understanding taxable reimbursement and old rules

Moving-related payments can affect your taxes in different ways, depending on who covered the expense and when the move happened. Here are a couple of rules to examine.

Employer reimbursement

Prior to 2018, employer-paid moving expenses were typically excluded from taxable wages, and employees could deduct additional amounts. Those rules are different now.

For most nonmilitary members, moving reimbursements are treated as taxable wages, which means the amount is included on Form W-2 and taxed like ordinary income. Since the federal deduction for moving expenses is currently suspended for civilian taxpayers, you generally can’t deduct out-of-pocket amounts to offset this income.

For qualifying service and intelligence members, reimbursements related to PCS orders may be excluded from income. If a reimbursement is excluded, you can still deduct any remaining costs. In that case, be sure to keep a detailed expense record, separating what you covered and what the government paid for.

Time and distance tests

Prior to the TCJA and OBBBA, the IRS used two tests to decide whether a job-related move qualified:

Time test: You needed to work full time at the new job for 39 weeks during the first 12 months after the move.

Distance test: The new work location had to be 50 miles farther from your former home than your old job was.

These tests don’t apply to active-duty service members claiming a deduction for a PCS move. But states choosing not to follow the OBBBA’s provisions might still use similar standards when determining whether moving expenses are deductible. So if you live in a state that has these rules, review the instructions carefully.

The process of deducting moving expenses on taxes

Eligible military households claim deductions on IRS Form 3903, and the form walks you through each calculation. First, list your deductible expenses, like transportation, storage, and lodging. Then, subtract any reimbursements that weren’t included in your income, and carry the net amount over to Schedule 1 (Form 1040) as an adjustment to income.

Tax software can complete the form for you, but you must retain documents like PCS orders, receipts from movers, and invoices from travel to support your claims.

For state-level deductions in qualifying locations, rules may vary. Reach out to a tax professional to confirm which forms to fill out and what information to provide.

Plan an affordable home purchase with Better

Today’s rules may limit who can deduct moving expenses, but this isn’t the only way to make your homebuying journey more affordable. Securing a favorable mortgage is one of the strongest ways to save money. To finance your new house while maintaining your budget, reach out to Better.

Our fully digital platform helps homebuyers save on their short and long-term budget. Compare mortgage rates with a few clicks to find the best interest available, improving your monthly payments for years to come. To save up to an additional $2,000 off closing costs, partner with a Better Real Estate agent and finance with Better Mortgage.

Simplify your homebuying experience with Better.

...in as little as 3 minutes – no credit impact

FAQ

Can I deduct moving expenses?

Yes, but only under specific circumstances. Members of the Armed Forces on active duty who moved because of a PCS can deduct certain items, including transportation and storage. Intelligence community employees also qualify.

At a federal level, civilians can’t deduct moving expenses. However, some states still allow deductions for job-related relocations.

What expenses are deductible for qualifying military?

For eligible service members, deductible moving expenses may include transportation of household goods, storage, and lodging for one trip. These amounts must be paid out of pocket, then deducted later.